“A cynic is a man who knows the price of everything, but the value of nothing; a sentimentalist

is a man who sees an absurd value in everything, but doesn’t know the market price of a single

thing.”

-Oscar Wilde

“Too many people spend money they haven’t earned to buy things they don’t want

to impress people they don’t like.”

-Will Rogers

“I love bringing that sparkle, the rainbow, and the sun to everything I do.”

-Paris Hilton

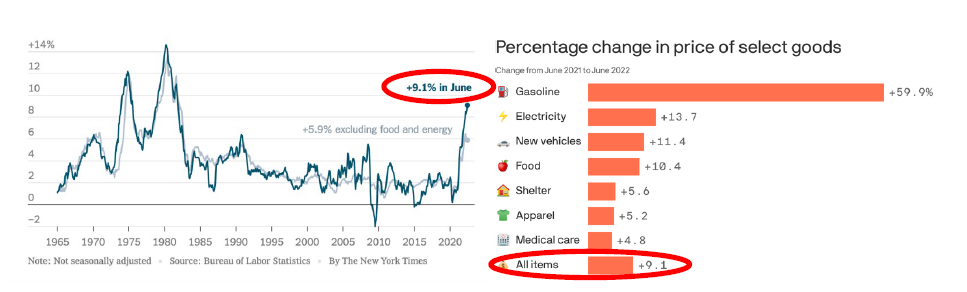

Some of you long-time readers of Clear Capital’s quarterly memos will recognize that

there are three quotes at the top of this letter as opposed to the typical two. Well, with

inflation being so widespread and of significant concern, especially following last

week’s report that the June Consumer Price Index reached another multi-decade high,

increasing 9.1% year-over-year, I decided, in sympathy, to inflate by 50% the number of

quotes with which I begin this quarter’s newsletter.

Besides, with so much tough news coming out of this quarter - from higher inflation to

significant increases in interest and mortgage rates, swooning equity and bond markets,

the specter of recession, the ongoing war in Ukraine, ever-growing gun violence,

shortages of baby formula, the (predictable) crash in the cryptocurrency markets,

sobering revelations from the January 6th Commission, controversial Supreme Court

rulings, to yet another rapidly spreading Covid subvariant – it hasn’t been a quarter

worth remembering or celebrating.

So why not start this memo with an uplifting, if not incomparably vapid quote from

Paris Hilton in an attempt to bring a “little sparkle, rainbow and sun” to an otherwise

forgettable quarter and an equally droll quarterly newsletter? Well, before I douse you

with too much sparkle and rainbow, here is a look at last week’s sobering inflation data:

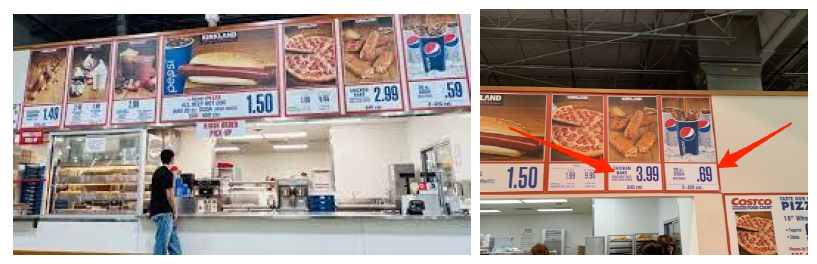

And as though the inflation story could not get any worse, I am still reeling from the

very recent announcement that Costco is raising some of their food court prices, with

the price of a chicken bake and a standalone soda being increased by $1.00 and $0.10,

respectively. The severity of the blow was tempered, however, by the welcome news

that they are not increasing the prices of either the hot dog/soda combination or the

price of their rotisserie chicken. Phew. If and when that happens, my faith in capitalism,

my Executive Costco membership, and view of life itself may collapse entirely.

So, it is for posterity and nostalgia’s sake (and a touch of sparkle and rainbow), that I

provide these important photos, to remind us of the way things used to be, them “good

ol’ days” and just how perverse inflation can be:

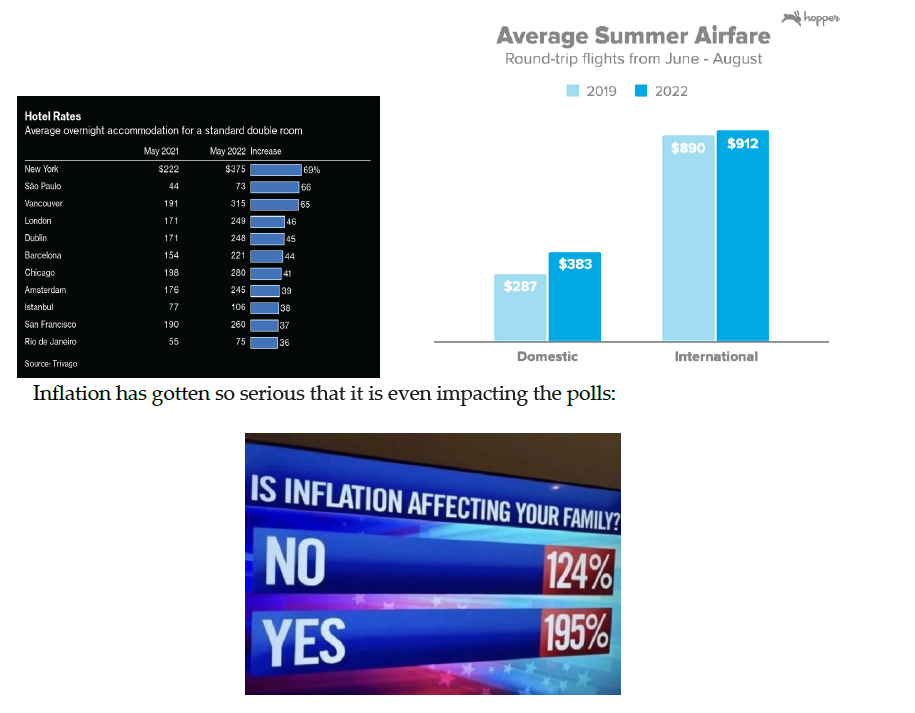

So, just how bad is inflation? Well, even family-owned Arizona Iced Tea, which had

stubbornly held onto its $0.99 price per can, announced this past week that it is

increasing the price of each can to $1.99, still less than its competitors, but one heck of

an increase. And how about the strongly rent-controlled City of Santa Monica,

affectionately and occasionally referred to by locals as the “People’s Republic of Santa

Monica,” approving the highest rent increase in 40 years, allowing landlords to hike

rents by six percent this year?

The two graphs below also confirm what many of us already know. Inflation has really

impacted travel costs, and we are not just talking about a gallon of gas.

Well, the Fed has not stood by idly, and following May’s inflation data (an 8.6% yearover-

year rise), Fed Chair Jerome Powell took a page out of Paul Volcker’s 1981 Federal

Reserve playbook, “How to Quell Inflation Regardless of the Consequences” and, along

with his colleagues, raised interest rates by 0.75%, the largest such increase since 1994.

Canada increased its discount rate by 100 bps (1%) last week, and most expect the U.S.

to follow suit with a similar increase later this month.

Keep in mind that Chairman Volcker faced far more daunting, double-digit inflation

when he was appointed Fed Chair in 1979. Inflation was rising at over one percent each

month and home mortgages averaged 11.2% at the time. The Fed Funds rate was just

under 11%, and by June of 1981, after a series of aggressive moves to quell inflation, the

Fed Funds rate exceeded…wait for it….19%. Imagine that. 19%.

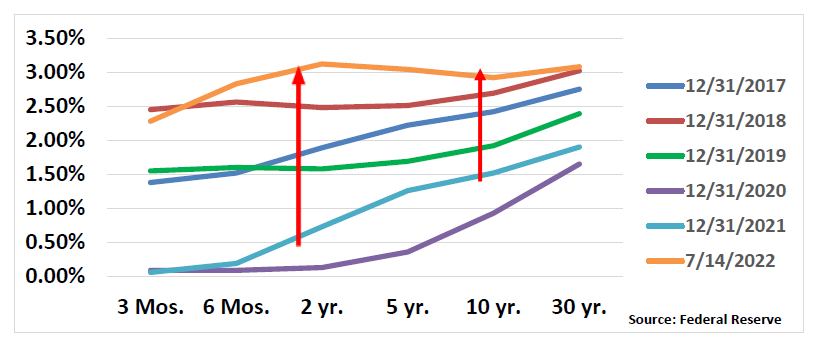

The response to the Fed’s recent actions has been predictable: a significant upward shift

in the yield curve, especially on the short (up to two years) end. Yields on two-year

Treasuries, which stood at 0.78% at the beginning of 2022, are now yielding 3.13%, a

more than fourfold increase.

And ten-year yields? They have increased to nearly 3.0% (2.93% at last glance), up from

1.63% at the end of 2021. Yes, you are reading the data correctly. Yields on two-year

Treasuries are currently yielding 20 bps (0.2%) more than those on ten-year bonds, at

least as of the end of last week.

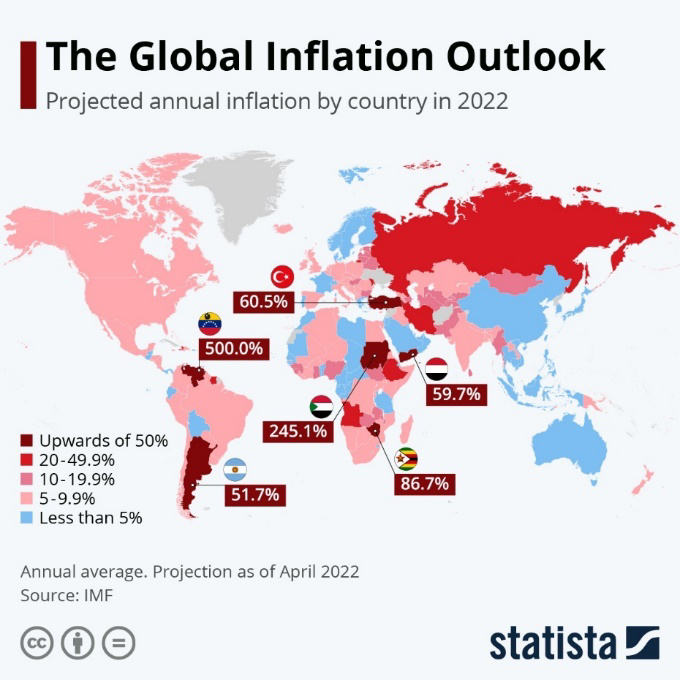

Oh, one last thing, though I am not sure it will make you feel any better. Despite all the

rhetoric and misplaced blame, inflation is a global phenomenon. Inflation in the EU has

been tracking slightly higher than that in the U.S. and many countries are experiencing

double-digit inflation.

What does this mean when short-term interest rates are higher than longer-term ones?

Is a recession imminent?

Inverted yield curves often precede a recession, and while the jury is still out on

whether we will experience a recession (two consecutive quarters of a drop in GDP),

investors and the markets are clearly expecting the U.S. economy to slow, to slow

dramatically, and for inflation and longer-term interest rates to subside as a result.

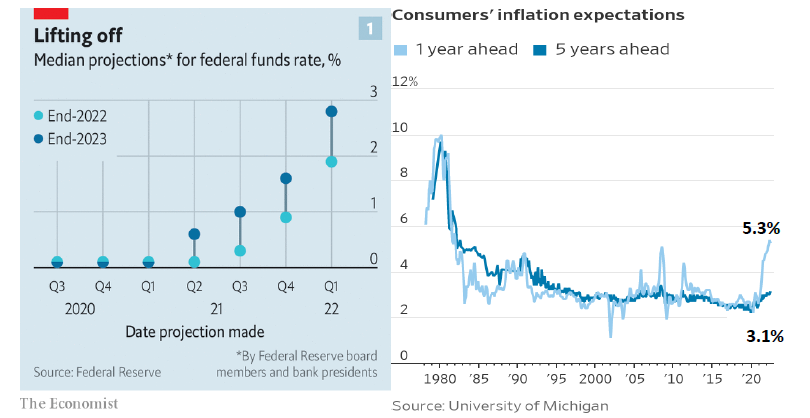

This conclusion is consistent with the following data, which indicate that while

investors expect short-term interest rates to continue to increase into 2023, they

anticipate that inflation will drop to near 3% within five years:

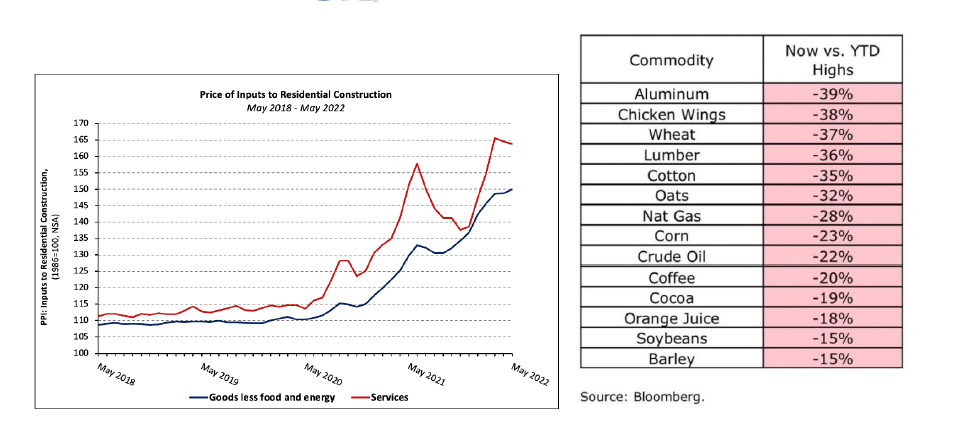

These predictions are not without some economic foundation. Since reaching an all-time

high last month, the average price for a gallon of gas in the U.S. is now about $4.50,

down from $4.84, while the prices for other commodities have declined significantly in

recent months. For example, copper prices just hit a two-year low and saw their largest

quarterly decline in over a decade. As the economy slows, recession or not, and short term

interest rates drop, future inflation rates should be tempered.

However, it will likely be some time before inflation approaches the Federal Reserve’s

two percent target, and while longer-term inflation may subside, one must wonder just

how much of the low inflation, low interest rate environment we have experienced for

the past several decades was simply a product of favorable demographics (i.e., slowing

population growth, reduced fertility rates), increased savings, globalization and the

shifts in production and outsourcing to places like India and China, automation,

Amazon, and aggressive fiscal policy.

And mortgage rates? What has been happening to real estate borrowing costs, and

what has been the impact?

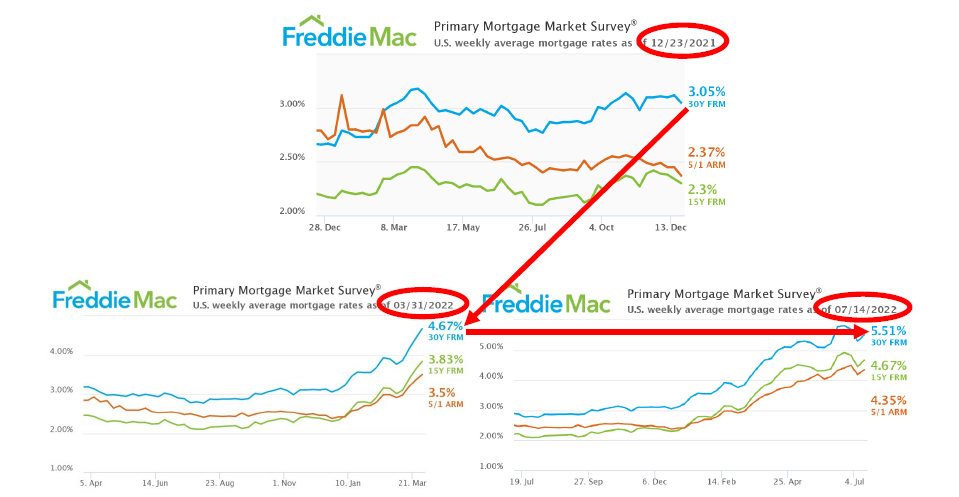

To nobody’s surprise, these too have spiked, though thankfully they have come down

from recent highs. It is hard to imagine that 30-year, fixed mortgage rates averaged less

than 3.0% in 2021 (2.96%, to be precise) and now exceed more than 5.5%, nearly

doubling in six months, and up nearly one percent since the end of the first quarter.

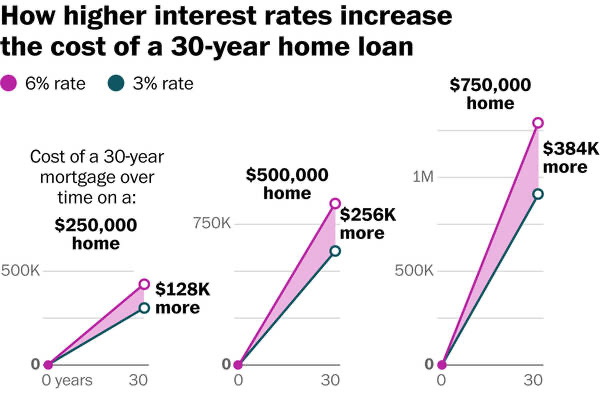

As a result, borrowing costs have increased significantly. The difference between a 30-

year fixed rate mortgage at 3% versus one at 6% translates to six figures or more in

additional (nominal) loan payments over time, depending on the price of the home and

size of the mortgage, of course:

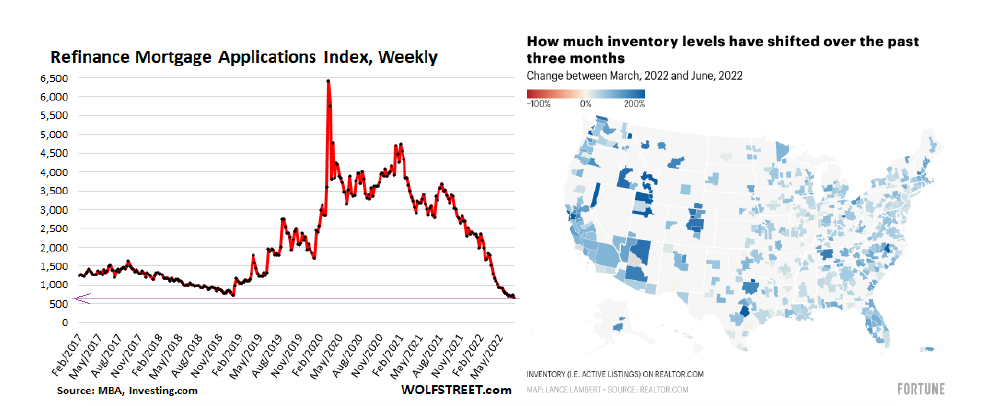

Again, to nobody’s surprise, mortgage applications for both new home purchases and

refinancings have plunged this year and the red-hot housing market has cooled, with

nationwide inventory of homes for sale up about 10% in recent weeks. Overall, in over

80% of the nation’s 400 largest housing markets, inventory levels have risen during the

past six weeks, although they remain below pre-pandemic levels.

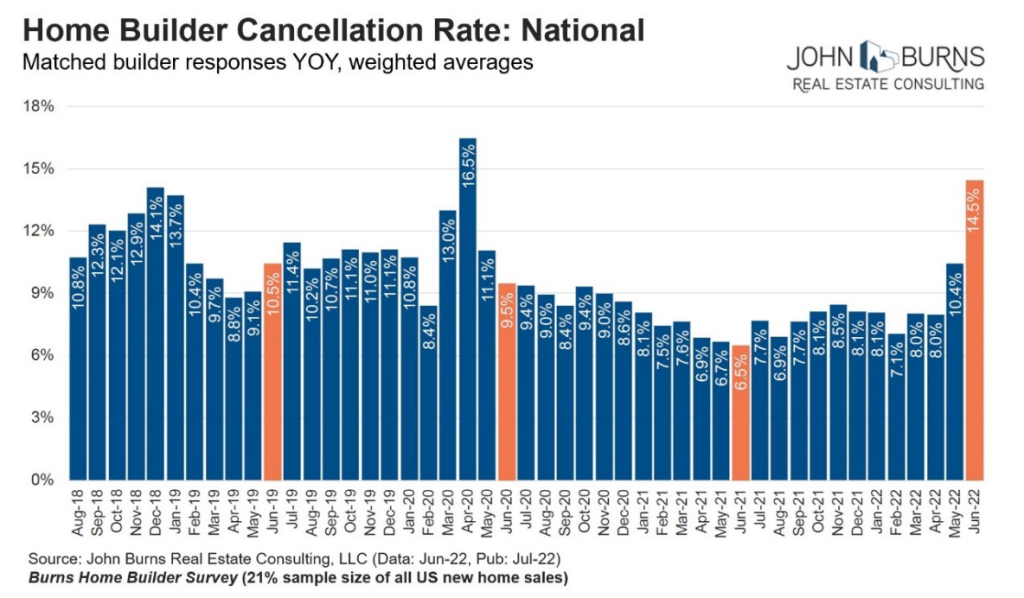

Finally, prospective homebuyers or those who have contracted with developers to

purchase new homes have been canceling those transactions in increasing numbers, but

these figures are not really alarming as cancellation rates are still less than what was

experienced at the start of the Covid-19 pandemic.

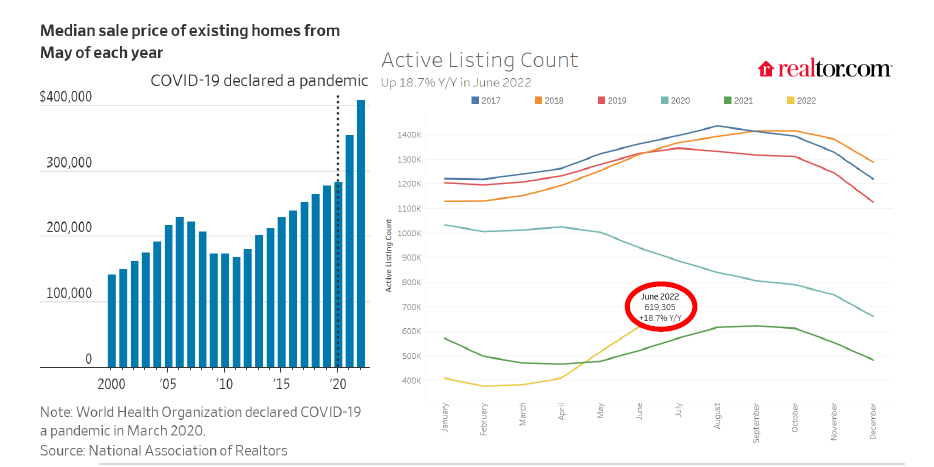

And housing prices? Have they dropped significantly in this environment of

substantially higher mortgage rates?

Well, this is where things get interesting and important. For the past several years,

prospective homebuyers have been fighting MMA-style for homes, like they were

chasing Beanie Babies, Cabbage Patch Dolls, or some other faddish holiday gift, rushing

into crowded Walmarts during Black Friday sales events. Buyers would send

compelling personalized letters and pictures of their families to accompany their offers,

believing that emotional connections might make the difference and compel a

homeowner to sell their home to them. Meanwhile, along with emotional pleas, these

potential home purchasers would foolishly agree to waive inspections and loan

contingencies, while accelerating closing dates, all caught up in the emotional frenzy.

However, while mortgage costs have increased and inventory levels risen (up almost

19% in June 2022 versus June of last year), home prices have not declined, at least not

broadly. That is, while demand has ebbed, supply increased, and prices in some

markets have softened, there was so much pent-up demand and liquidity awaiting

investment, such that these demand drivers coupled with an overall lack of supply and

persistent underbuilding, prices on closed transactions continue to rise overall. I don’t

believe this trend to be sustainable and prices will inevitably decline, at least in some

markets, especially those at the very high-end (e.g., San Jose, Seattle) or where prices

rose the most in recent years (e.g., Boise, Fresno).

However, I expect home prices overall to drop only modestly, perhaps five to 10

percent, and in some markets, prices may not fall at all. Liquidity on the sidelines

remains high (M2 money supply stood at about $21.75 trillion at the end of May),

institutions are likely to continue their purchases of homes to rent (institutions

accounting for 20% of all home purchases in the last quarter of 2021), household

finances and debt levels remain in decent shape, banks remain adequately capitalized

and, having learned their lessons from the Great Financial Crisis, have significantly

tightened up their borrower underwriting (average FICO scores for homebuyers and

borrowers are about 50 points higher than what preceded the financial crisis).

Perhaps prospective sellers will merely see fewer offers, fewer family photos and

handwritten emotional pleas, and may simply receive more customary purchase offers,

you know, the kind which include due diligence provisions, contingency periods, and

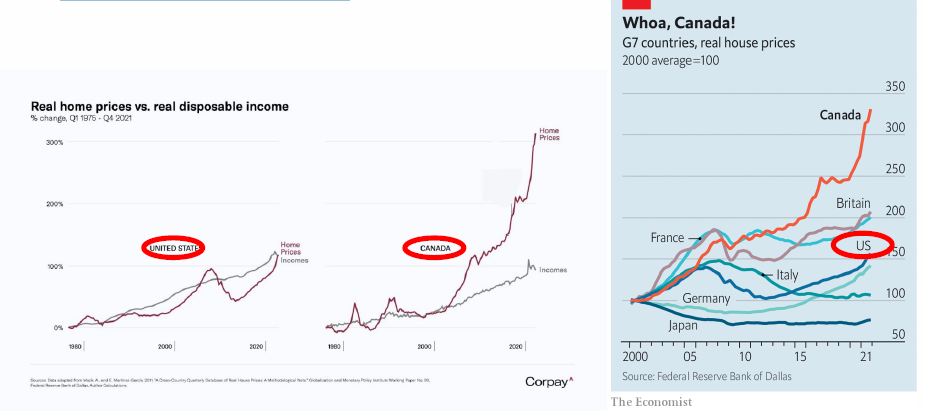

closing dates. Frankly, I would be far more worried about the single-family housing

markets if I were Canadian, British, or French. In those markets, prices have risen far

above disposable income levels:

And multifamily rents and occupancies? How have apartments fared in this higher

interest and mortgage rate environment?

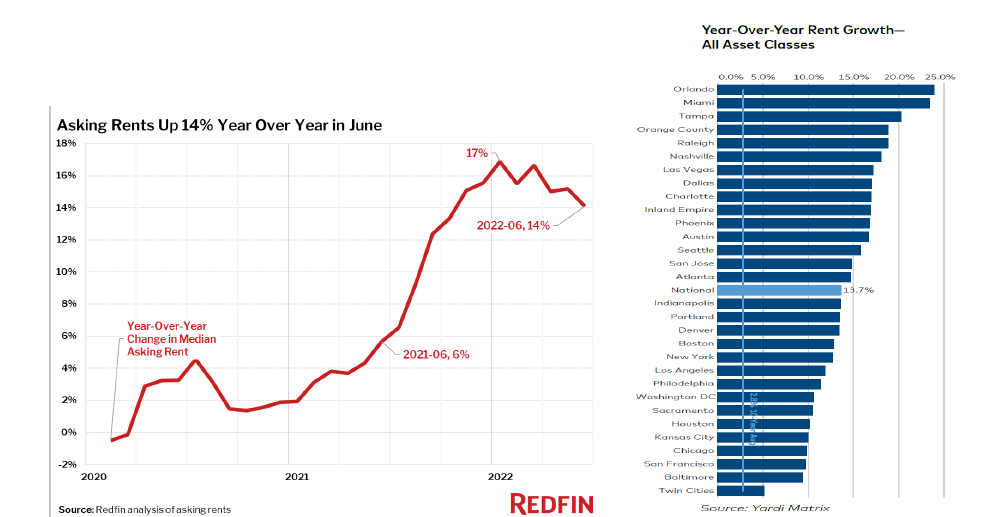

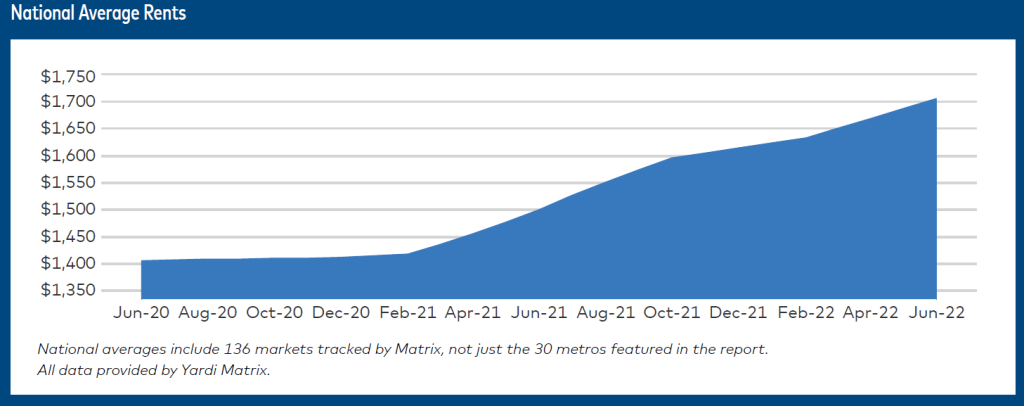

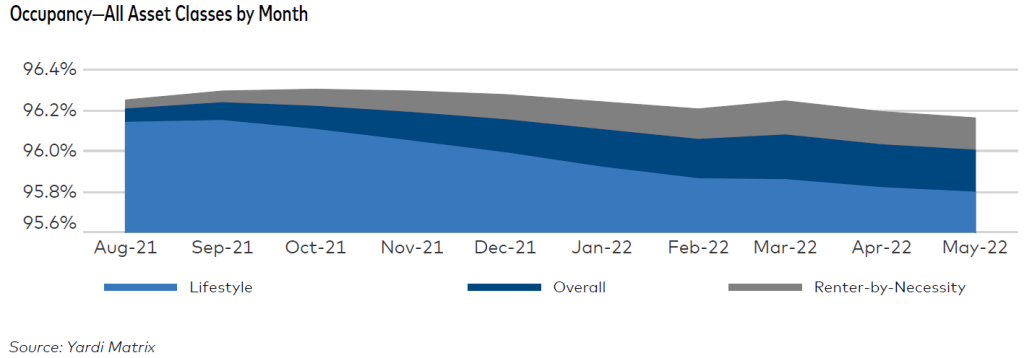

Well, in two words, “very well,” and being that I am big on pictures telling 1,000 words

(actually 1,500 now, due to inflation), here are three telling graphs:

Meanwhile, occupancy rates nationally remain above 95%, consistent across asset quality and

location:

Through June, rents rose 14 to 15% nationally year-over-year, with the median listed

rent for an available apartment rising above $2,000 a month for the first time. Rents are

up more than 20% in several Florida markets (e.g., Orlando, Miami, and Tampa) and

over 15% in many markets (e.g., Austin, Phoenix, Nashville). Across the Clear Capital

portfolio, rents are up more than 10%, and higher in certain markets and in certain

assets. The only residential asset in the country with substantially declining rents is the

Arconia in New York City, due to the high number of violent crimes and unsolved

murders that continue to happen there (shameless plug for “Murders in the Building”

for you fans and Hulu subscribers).

While bidding wars have been a staple of hot single-family markets, these contests are

becoming more commonplace in the rental market. Real-estate agents from New York

to Chicago to Atlanta say they see more people than ever making offers above asking to

lease homes and apartments that they will never own. An increasing number of whitecollar

professionals—some of whom recently sold homes—are reluctant to buy or buy

again because of record-high home prices, those higher mortgage rates, and limited

supply of homes for sale. They are renting instead, helping to drive a frenzy for leased

properties of all kinds, and helping fuel the higher rent trend.

Look, the math is simple. If more folks - whether blue-collar or white, whether single or

married, whether childless or not - enter already hot markets where home prices and

mortgage rates remain high and where the supply of new homes for them to rent or buy

doesn’t substantially increase, rents really have nowhere to go, but up. It’s a simple

process. Mortgage rates go up, the ability for homebuyers to purchase homes decreases

(much higher down payments required along with higher ongoing servicing costs), and

there are more renters in the market who will remain renters for longer periods of time. In the face of static or modestly increasing supply, rents increase.

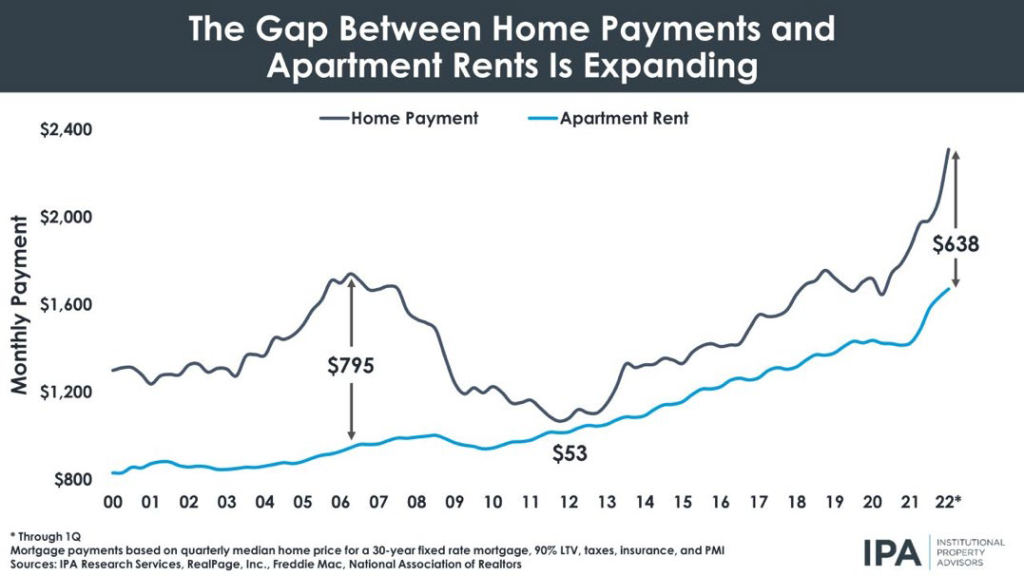

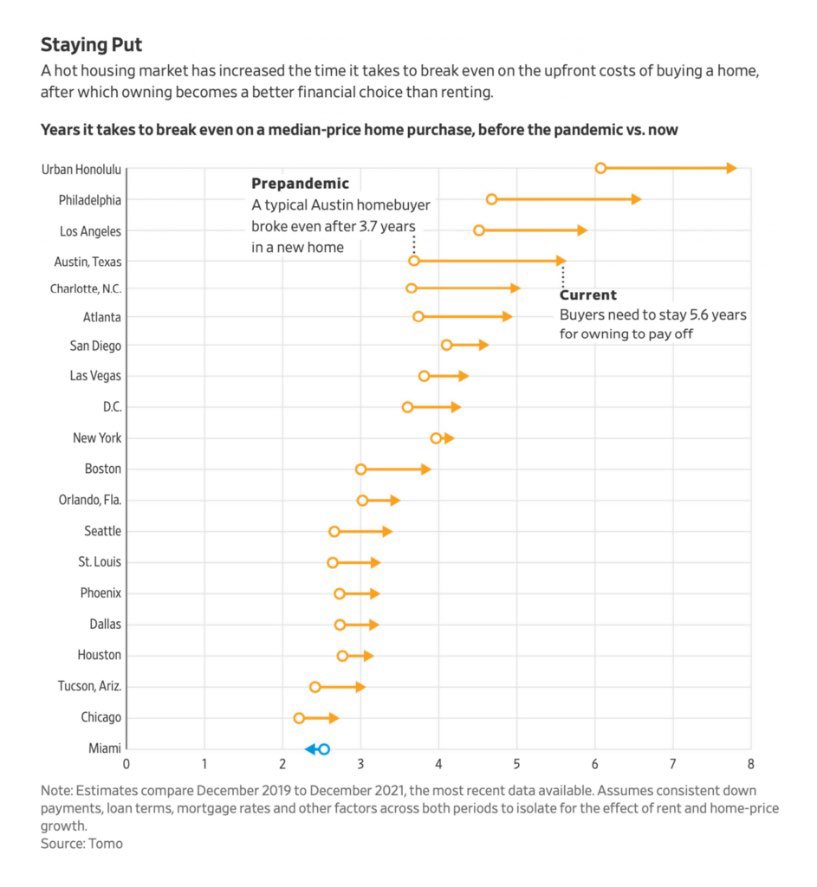

Yet, even as rents have risen, the cost of owning has increased even more such that gap

between the costs of owning and renting has widened:

In many cities, home prices have increased so much that the time it takes to “break even” on a

home purchase (due to the higher upfront and ongoing mortgage costs) has widened, making

renting more attractive. For example, in Phoenix, where Clear Capital owns six assets, it now

takes over three years to break even on a median-price home purchase, up from about 2.5

years it took before the pandemic.

While builders were completing units at an unusually rapid rate in early 2022 (349,000

units per-year), about 1.2 times the pre-pandemic pace, according to the Joint Center for

Housing Studies at Harvard, the number of occupied apartments was rising more than

twice as quickly. For now, the housing market is bifurcating, with the market for

purchased homes slowing even as the rental market remains hot. Already, new home

construction has dropped sharply as borrowing costs climb, declining 14.4 percent in

May to the lowest rate in more than a year. Early data suggest that apartment

construction is also being impacted.

The caption from a recent WSJ article (late June) - “Worker Shortage Stymies

Construction” - highlighted one of the issues impeding the addition of new supply to

the constrained market. With unemployment already low (see additional discussion

below), homebuilders and contractors cannot identify and hire enough help, a challenge

exacerbated by the demand for labor tied to $600 billion in transportation-specific

funding earmarked in the $1.2 trillion bipartisan infrastructure bill passed last

November.

So, short-term residential housing data in this inflationary environment looks

favorable, but what are the prospects longer-term?

Because short-term trends can deceive, the question as to how investments in real estate

perform longer-term in the face of high inflation is an important one and was the

primary focus of our most recent monthly newsletter Clear Insights. Without repeating

all that was discussed there, I will simply provide a few data points and graphs that

were included in the newsletter in case you missed it.

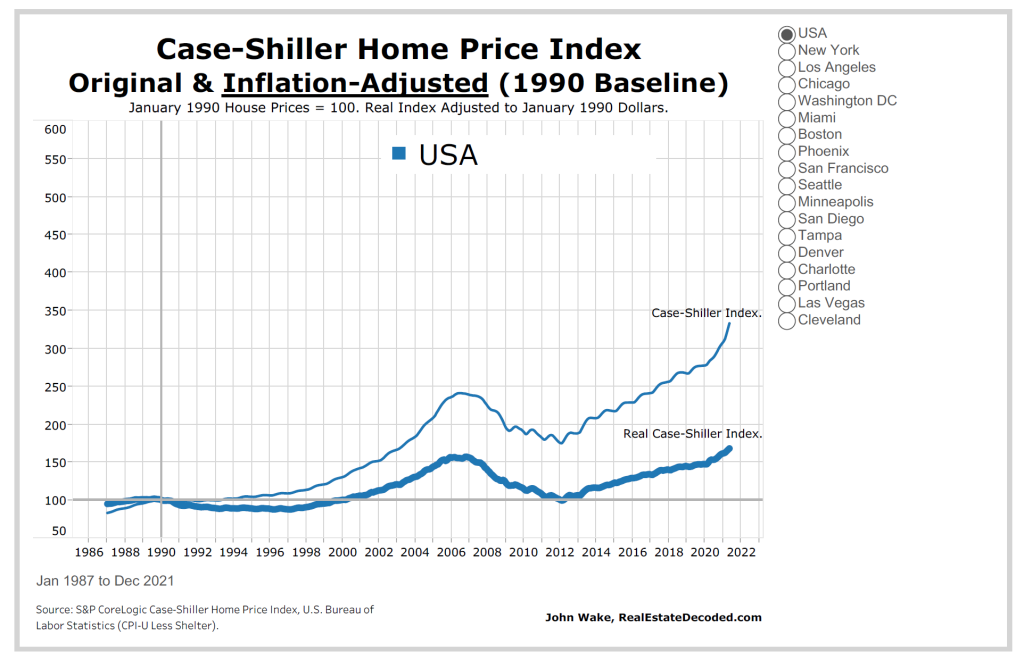

The first demonstrates that single-family homes have provided positive real returns

(above inflation) since 1990.

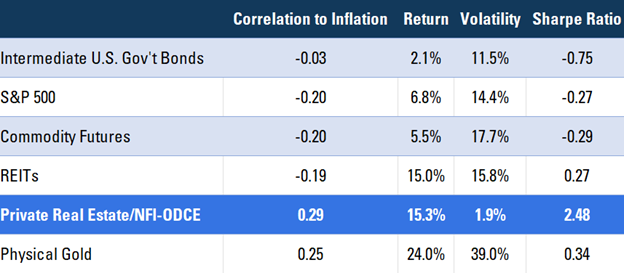

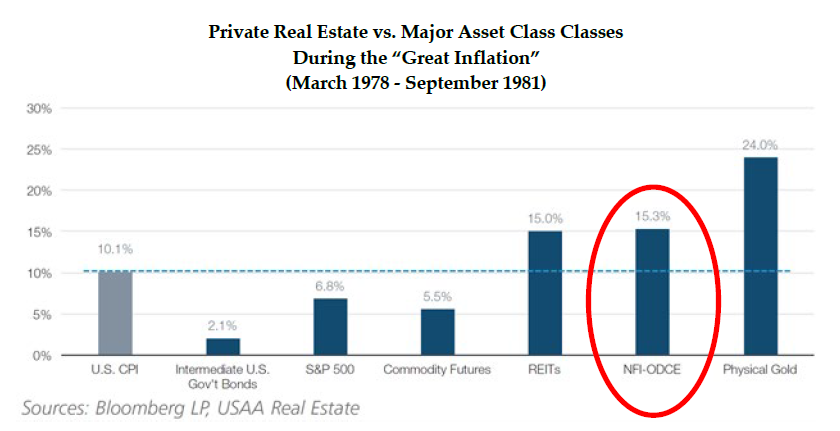

Meanwhile, during 1978 to 1981, a period some refer to as the “Great Inflation,” private

real estate exhibited the highest correlation to headline inflation of all major asset

classes. Private real estate also had the most favorable risk-adjusted return profile

during this period, as illustrated below.

Private Real Estate vs. Major Asset Class Classes

During the “Great Inflation”

(March 1978 - September 1981)1

Finally, a paper published in November 2011, “Inflation and Real Estate Investments,”

written by Brad Case, Senior Vice President of NAREIT, and Susan Wachter, Professor

at Wharton, evaluated how publicly traded Real Estate Investment Trusts (REITs), the

most transparent of real estate investments, and came to a similar conclusion. In 1979,

when the consumer price index averaged 13.5%, total REIT returns 24.4%. During 1978

to 1980, when inflation averaged 11.6%, REITS’ total returns were 23.1%, and from 1974

to 1981, when the CPI averaged 9.3% per year, REITs returned 16.3% on average.

In theory, multifamily investments ought to perform well in an inflationary, high

interest-rate environment because of their shorter-term lease structures and higher

demand versus single-family homes, the latter of which become substantially less

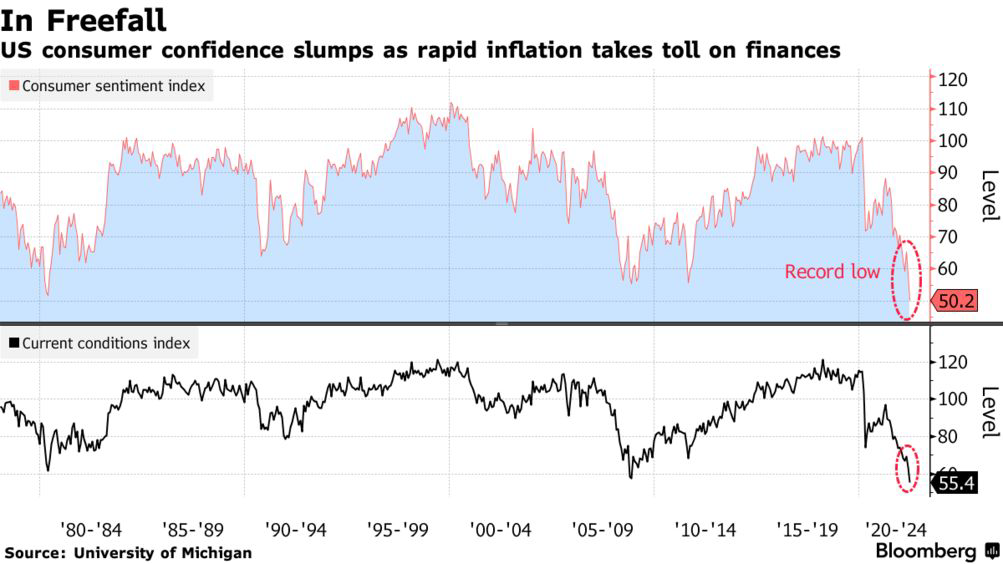

affordable, as set forth above. In addition, in the face of greater uncertainty and risk,

prospective homebuyers prefer to sit on the sidelines and wait. After all, homebuying

activity may represent the single best barometer of consumer confidence, given it is

such a substantial and generally illiquid investment. And consumers are not exactly

brimming with confidence these days, which cannot come as any real surprise.

Even with the decline in confidence, consumers can carry on spending for a while, as

households across developed countries are still sitting on roughly $4 trillion of savings,

about 8% of GDP, mostly due to savings and government largesse during the

pandemic. To be clear it is not just the well-heeled who have increased their savings. I

read an interesting statistic recently that bank accounts of lower-income families were

65% higher than end of 2021 vs. 2019. Cynics will rightly point out that this statistic is

deceiving given the low absolute level of savings in this lower-income demographic, a reasonable criticism, but the broader point remains. Households are in better financial

shape than they were before the pandemic, all else equal.

Finally, with average hourly earnings for private-sector jobs increasing about five

percent in 2022 (the highest increase in years), these higher wages, while below inflation

and inadequate to shrink the mortgage cost-rental gap, will still allow for greater rental

payments. Moreover, I anticipate that even higher wages are forthcoming as employers

seek to fill open positions.

Meanwhile, there are a couple other issues and data points regarding housing

worth discussing

• “The Great Reshuffling” (not to be confused with the “Great Resignation”):

According to a new working paper from the National Bureau of Economic

Research, written by researchers from the Federal Reserve Bank of San Francisco

and the University of California, San Diego, home prices grew by nearly 24%

during the pandemic (December 2019 through November of last year), and the

study found that remote work accounted for 15.1% (or 60% on a relative basis) of

that growth. Cities like Austin, Boise, Phoenix, and San Diego saw some of the

biggest home prices increases in the country as a result.

According to the study, these remote-work friendly cities share three principal

features: i) A predominant industry that allows for remote work. Tech jobs, for

example, can often be performed remotely because they mostly involve work on

computers, of course; ii) Lower population density, where there is more space

and more affordable housing than in the biggest cities in the country. Because of

the high living costs in Manhattan, for example, having extra space for a home

office comes at a significant premium, even if it is economically doable. Lowerdensity

areas are more attractive for remote work; and iii) A warmer climate or

appealing lifestyle. I know this is a real shocker, but folks working remotely

would rather hear ocean waves, singing birds, and croaking toads (Jim Croce,

anyone?) than horns honking, trucks beeping, and sirens wailing.

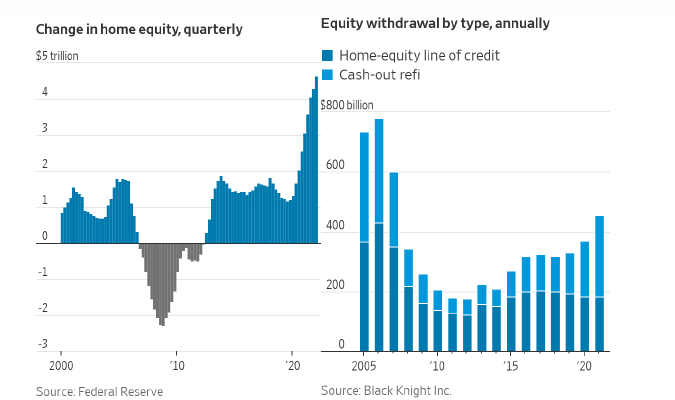

• Increased amounts of home equity: According to the Federal Reserve,

Americans have more equity tied up in their homes than ever, nearly $28 trillion,

up over $4.5 trillion during just the first quarter of 2022. The hot housing markets

are largely responsible, of course, along with the high concentration and longterm

ownership of single-family homes by Baby Boomers who are reluctant or

unwilling to sell.

What is interesting is that a significant chunk of that increased equity has been

monetized through cash-out refinancings or HELOCs (home equity lines of

credit). There is no question that this additional liquidity found its way into the

markets and compelled increased economic activity. This source of economic

lighter fluid will all but dry up this year.

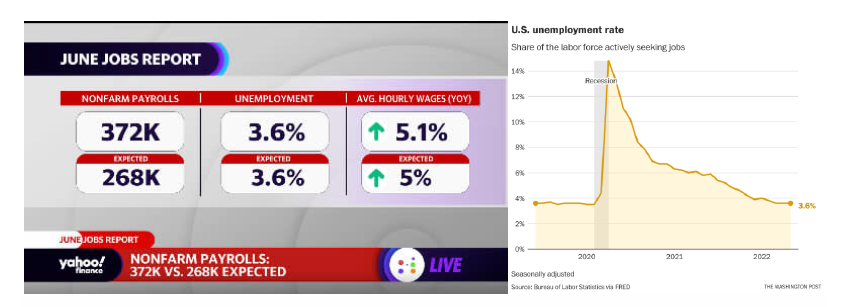

One bright spot is the job market, which remains surprisingly robust

Last week, the Bureau of Labor and Statistics indicated that non-farm payrolls increased

372,000 in June, well above the 268,000 estimate, maintaining the unemployment rate at

3.6%. Meanwhile, there are still over 11 million job openings, and anecdotally, many

businesses are having difficulty attracting and retaining help. Thus, although we may

experience a recession later this year or next, an economic downturn may not result in

significant job losses, net-net. While job losses may accelerate in some industries with

softening growth (e.g., tech, retail), other industries may very well see continued job

growth (e.g., travel and hospitality, construction).

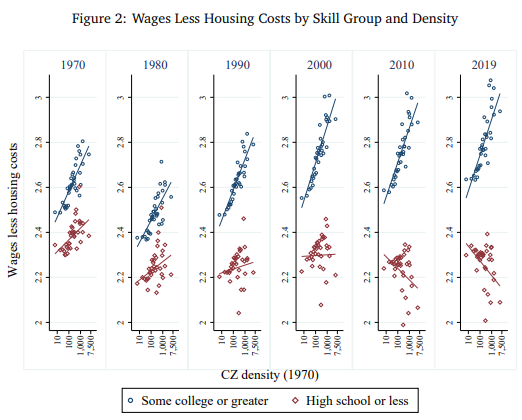

There were a couple of academic research papers that recently caught my eye, each

focusing on different issues involving labor and housing. The first was “Low-Income

Workers, Residential Location, and the Changing Commute in the United States;” and

the second, “Moving to Density: Half a Century of Housing Costs and Wage Premia.”

Imagine you are a janitor, an important but lower-level employee. Would you be better

off economically if you lived and worked in Huntsville, Alabama, or New York City?

What about if you are an MBA-trained investment banker or an attorney? How far

would (or should) such a worker commute to get to their job? How does the cost of

housing impact answers to these questions? Have workers stopped moving to the

highest-density, highest-productivity places in the country because of a decline in the

urban wage premium, or because the rent is too high? These two papers tackled these

sorts of questions, made interesting observations, and asked thought-provoking policy

questions.

Typically, lower-income workers lived closer to their work and had shorter commutes,

often working and residing in high-density urban cores. These non-college workers

earned “urban wage premiums,” benefitting from the proximity between their

residences and places of employment. Higher wage earners generally live in the

suburbs and make longer commutes to work, on average, but also benefitted from an

“urban wage premium” because employers would pay premia for employee skills. This

all seems intuitive.

However, the authors found that a growing number of lower-income workers have

relocated to the suburbs in search of more affordable housing, which increases

commute times. In some cases, work had indeed shifted from the urban cores to the

burbs, but more often than not, the cost of housing was a key factor in the relocation. In

short, the “urban wage premium” for unskilled labor is now an “urban wage penalty”

because housing costs are too high. This shift creates real challenges, especially for

businesses in urban cores that rely heavily on unskilled labor. How are such businesses

going to attract and retain needed workers, especially if reliable and efficient public

transportation isn’t available? Are employers going to need to provide and/or or

subsidize the cost of transportation to employees? Should the government subsidize

these efforts?

Looking forward, the lack of affordable housing and spotty public transportation in

many communities is going to create significant challenges to businesses in certain

urban cores that rely on unskilled labor, with such challenges only exacerbated by the

pandemic.

Perhaps one of the related issues is the disparity between average worker pay and

management. In another article I recently read, I was not at all surprised to learn that

even with the recent increase in worker wages, which are up about six percent this past

year, it would take 186 years for the average worker at a publicly traded company to

match what a typical CEO earns. 186 years, about how long it has been since my

beloved Bruins appeared in a meaningful Bowl game.

In 2021, the typical compensation for the CEO of an S&P 500 company was up more

than 17%, to a median of $14.5 million. Obviously, some executive compensation

packages are eye-popping. The CEO of Expedia Group took down a cool $296.2 million

last year, while Jamie Dimon of JP Morgan Chase earned a mere $84.4 million. In

comparison, the median Walmart Associate made $25,335 last year. I suppose it is no

wonder that workers are making increased efforts to unionize, with employees of

Amazon and Starbucks garnering the most attention in recent years.

While the second quarter was reasonably quiet in terms of new housing regulations,

that would change significantly if John Oliver had his way,

Some of you may have seen the John Oliver segment from late June where he focused

on rising rents and housing affordability and argued that housing should be a federally

funded right and rent control broadly expanded. Landlords were essentially portrayed

as greedy capitalists raising rents mercilessly at the expense of the working class. You

can check it out here, if you are so inclined:

https://www.bing.com/videos/search?q=john+oliver+rent+control+you+tube&docid=608052449075874575

&mid=FF11ADDEF511F1CDADEBFF11ADDEF511F1CDADEB&view=detail&FORM=VIRE

Now, as much as I like a lot of John Oliver’s schtick and enjoy thoughtful comedy and

commentary as much as anyone, I was profoundly disappointed at how superficial,

incomplete, and fundamentally flawed his analysis and conclusions were. I realize that

Mr. Oliver hosts a comedy show, and as a comedian, he might not have all his facts

right or understand all the nuances on a topic he covers. But he barely touched upon

issues surrounding the supply of housing, excessive regulation, byzantine building

codes, and public opposition to almost any proposed project, especially those with high

density. It is what an experienced litigator feels when watching an episode of “Law and

Order.”

In one obvious error, Oliver rails on new construction, complaining that it is only

directed to high-end, white-collar renters, and that this new supply does not help the

working class and their need for housing. On the macro-point, of course he is right. We

need more darn housing and more affordable housing. But his analysis is flatly

incorrect and way too shallow. All else equal, more housing supply means more

available housing and lower overall rents, period. Additional supply of higher-end

units will allow some white-collar renters to relocate from their Class B units, making

them available to more cash-strapped renters.

He fails to mention that affordable housing projects require government largesse, which

is not only limited, but comes at a price. Complying with all the rules and regulations

tied to whatever government largesse is received (i.e., need to use unionized labor,

comply with stricter environmental regulations) substantially increases the cost to

construct affordable housing projects. More than half a dozen affordable projects here in

California are costing more than $1 million per unit, three times what it costs to build a

market-based unit.

In another glaring oversight, he was wrong on rent stabilization, claiming that it only

exists in California and Oregon. He failed to mention New York and its two types of

programs: rent control and rent stabilization. He failed to mention that some form of

rent control exists in other jurisdictions, from Boston to Minneapolis to Washington

D.C. Finally, he claimed that many landlords refuse to accept Section 8 vouchers, which

is true, but misleading. In California, for example, a landlord may not discriminate

against a prospective Section 8 tenant and may not reject them out of hand. If a unit is

available and a Section 8 tenant comes along and otherwise qualifies as a renter, the

landlord has to rent to that Section 8 tenant.

Finally, this quarter’s winner for least effective public policy decision to address

housing affordability goes to a regular nominee for the award, the Los Angeles City

Council, which voted 12-0 to purchase and municipalize a 124-unit property just north

of downtown and Chinatown to prevent the current landlord from increasing rents to

market. On the one hand, I applaud the landlord for creating enough of an uproar to

compel the City to purchase the property from him at its fair value. On the other, I am

none too thrilled that taxpayer funds (to which I am a contributor) are being used in

such an ineffective way, one that will make absolutely no meaningful inroads to the

housing affordability challenges the City faces.

Before we put another quarterly memo to bed, I should mention a few other events

impacting financial markets and the economy

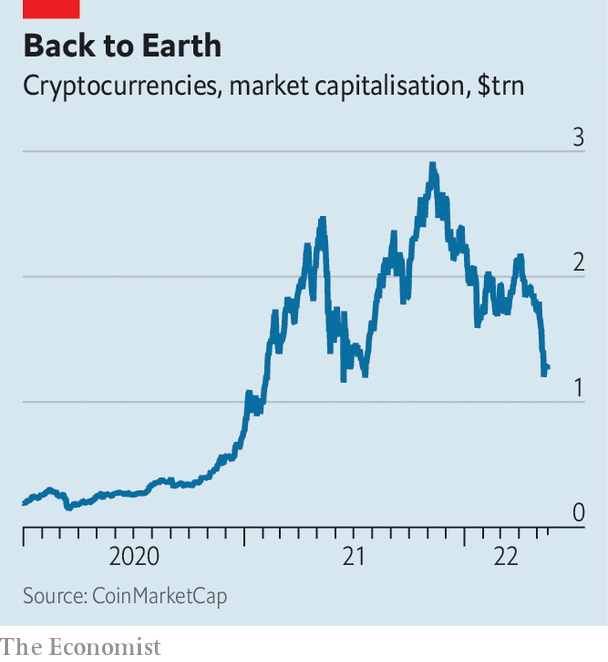

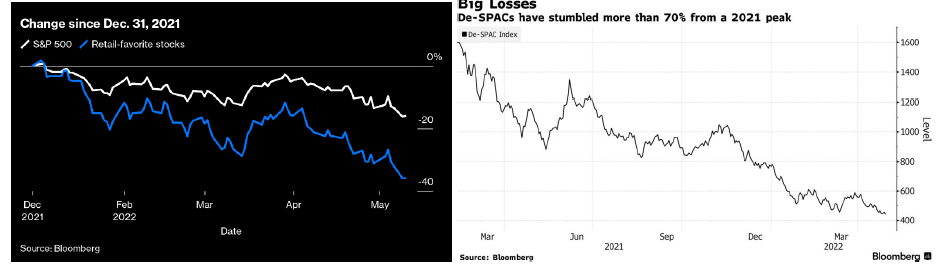

• Cryptocurrencies and other speculative investments (e.g., Meme stocks,

SPACS) have their comeuppance. This quarter saw the implosion of the

cryptocurrency market, with the total capitalization of Bitcoin and its siblings

losing almost $2 trillion (over 60%) in value, and frankly, as much as I hate for

anyone to lose money, if not their life savings, it has been long overdue. As I

discussed in one of my Focus on Facts podcast episodes last year (still available

on Spotify and Apple!), “Bitcoin: Currency of the Future or Just Another

Bubble?,” I could never discern a compelling need for cryptocurrencies, at least

for non-illicit transactions and honest transactors. Deregulated markets coupled

with human propensity for greed are a toxic cocktail. Other speculative

investments (read: meme stocks, SPACs) took it on the chin in the second

quarter.

Several crypto exchanges, dealers, asset managers, and lenders ironically now

occupy crypts, having filed Chapter 11 during just the past couple of months -

Voyager Digital, Three Arrows, Celsius – while a number of “stablecoins” (can

you say “oxymoron”?) proved anything but (e.g., Terra/Luna). With more crypto

firms becoming insolvent and filing for bankruptcy, it is now clear that many

customers (gamblers?) will face massive losses, and another generation will have

learned a painful lesson and the difference between investing and speculating,

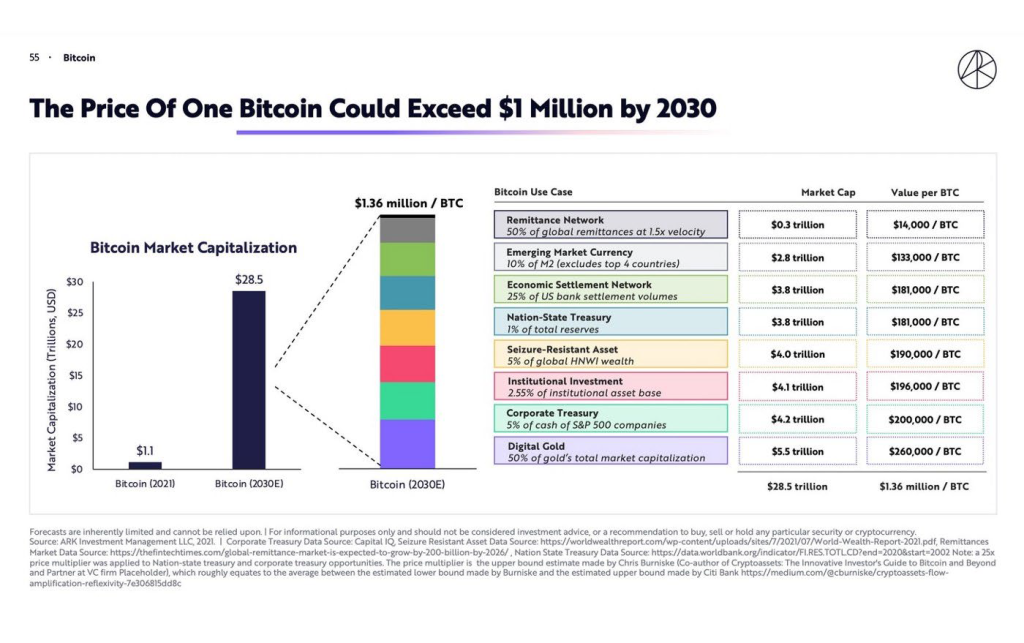

and how silly graphics like this, which seem polished, are nothing more than

graphical artistry and a paragon of “form over substance.”

• Strength in the U.S. Dollar: Perhaps not completely untethered (pun intended)

from the collapse in the cryptocurrency market, the dollar is up by over 7%

during the last twelve months, versus a broad basket of currencies, and is now

trading at par (1:1) with the Euro for the first time in 20 years. Slowing economic

growth, exacerbated by an energy crisis brought on by the conflict in Ukraine

and high inflation (the EU’s inflation rate is close to our own), has seriously

impaired the value of the Euro. This is good news for those of you intending to

travel to Europe this year but not so great news for global economic stability and

financial markets generally.

Finally, history tells us that markets cannot be timed, with peaks and troughs known

only in hindsight. Therefore, most investors should simply stay the course, effectively

managing leverage and focusing on investing in assets that should do well in

inflationary environments.

It is hard to sugarcoat the news and challenges that the second quarter brought, making

it no easy task to watch or read the headlines: higher inflation and mortgage rates,

declining stock markets, geopolitical conflicts, increasing threat of recession, gun

violence, another virulent variant of Covid, the crash in crypto and other speculative

assets, sobering revelations from the January 6th Commission, food shortages globally

and a baby formula shortage closer to home. At this point, newscasts should start their

broadcasts with health warnings like those for pharmaceutical products: “This news

report may cause gastrointestinal distress, increases in blood pressure, and difficulty

with breathing.”

However, as I mentioned in our last quarterly memo, markets and investor sentiment

are fickle things, and it is a fool’s errand to chase what’s hot and sell what’s cold in an

effort to time peaks and troughs in asset values. If pictures tell 1,000 (I mean, 1,500, due

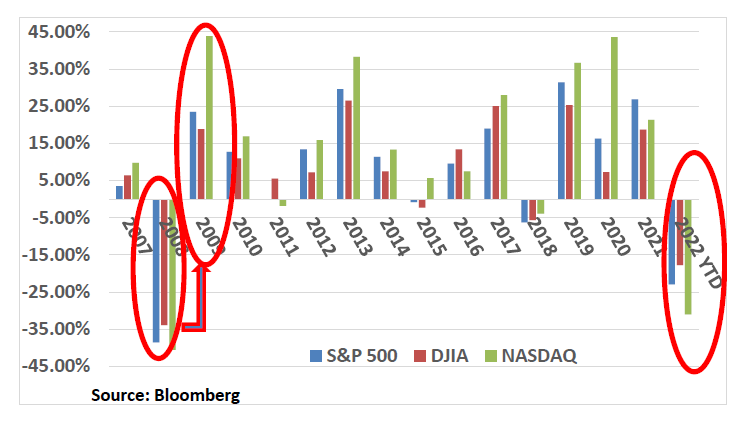

to inflation) words in this regard, these have to do the trick:

I want you to imagine that you are back in 2009, and reliving the Great Recession, when

equity prices fell nearly 40%. What was your mindset then? How eager were you to

make new investments at that time? Were any of us predicting that the market would

bounce back the following year? Well, it did, and the next decade was incredibly

favorable for stock prices. How long after the Great Financial Crisis ended were you

making investments without even giving any thought to what had happened not much

earlier? 2011? 2012? Most likely it was after the markets had already recaptured much of

their losses.

Fast forward to today, when the S&P 500 and NASDAQ are down approximately 19%

and 27%, respectively, during just the first half of 2022. I imagine many of us are

nervous, hoarding cash, and awaiting markets and asset prices to stabilize before

jumping back in. Well, if history is any indicator, by the time that happens, you will

either be late to the party or will have missed it entirely. Obviously, I cannot predict

that equity markets will bounce back during the second half of the year or in 2023, but I

sure wouldn’t bet against it. Rainbow, sparkle, and sunshine are always around the

proverbial corner. Just ask Paris Hilton if you don’t believe me.

Meanwhile, Clear Capital continues to execute, maximizing returns on its existing

portfolio, and pursuing acquisitions we find attractive, including Aspire West Phoenix,

an 180-unit project built in 1977, with attractive fundamentals and projected returns.

Details about the offering can be found here:

https://investors.clearcapllc.com/portal/offering/8fedb2db-5fc7-47ff-a598-c881f6e80537.

We will close our fundraising for this asset in less than two weeks, so let us know if you

might be interested or want to learn more. We anticipate refinancing and/or selling a

handful of assets before the end of the year, so stay tuned for additional news on that

front.

And lastly, because I do want to end a droll quarter and lengthy newsletter with some

Paris Hilton inspired positivity, I will turn to my go-to therapy in tough times and

favorite life advisors and philosophers, Calvin & Hobbes, who never disappoint.

With that, the entire Clear Capital team and I pass along our very best wishes to you

and yours, and hope you make the most of your remaining summers, just like Calvin

and his stuffed tiger companion.

We thank you for your continued engagement and support of our firm and its

endeavors, including our latest opportunity, Aspire West Phoenix. And, as always, I

want to express a special round of thanks to the Clear Capital Team, who continue to go

above and beyond for our clients, colleagues, and partners.

Best,

Eric Sussman

Managing Partner