“What a Long Strange Trip It’s Been”

– Grateful Dead“It is often said that there are two types of forecasts…lucky or wrong”

– Anonymous

During this past quarter, there were more than a handful of times that I read a particular headline and did a double take, just to make sure that I was actually reading the Wall Street Journal, Bloomberg, or other article from the mainstream news and not the Onion or similarly satirical news source.

In March, the Los Angeles Times had an article captioned: “Hottest Housing Market? It’s Fresno.” With no disrespect to Fresno, located in Central California’s San Joaquin Valley, the words “hot,” “housing market,” and “Fresno” do not usually appear in the same sentence. Yet, Fresno is just that when it comes to real estate prices and rents. Hot. The median rent in Fresno was up 12% during the last year, one of the top markets in the nation, and a modest single-family home that recently went up for sale there received over 100 offers, many offering all cash. In fact, Fresno, and cities like it throughout the Southwest, Sunbelt, and Mountain West – from Fresno to Boise to Gilbert (Arizona) to Riverside (California) – have been some of the strongest the past year, all benefitting from the pandemic, low interest rates, and more modest housing costs.

Then there was this doozy from CNBC in early April: “Paris Hilton is Fascinated by NFTs and Very, Very Excited About Bitcoin.” I have previously joked that when your Uber driver, barber, or gardener shares an investment idea with you, we just might be at a market top. However, I am sure Paris Hilton’s interest in Non-Fungible Tokens (digital art) and cryptocurrency is different, a uniquely bullish sign. #sarcasm. Then again, a digital collage – a Non-fungible Token – sold for a record, $69 million during the quarter, so perhaps Ms. Hilton is really onto something.

And then there was this classic from Bloomberg, which appeared a couple of days ago, “Everyone Loves the $100 Million Deli, Except David Einhorn,” about a rural New Jersey deli, which went public (symbol, “HWIN”) and, despite less than $14,000 in 2020 revenues, sports a market capitalization of over $100 million (actually $102 million at last glance, and if you include its outstanding warrants, over $1 billion), capturing the attention and cynicism of Mr. Einhorn, a well-known value investor and fund manager. Clearly, his value focus fails to appreciate the growth opportunities and potential in pastrami and corned beef. Imagine if this deli accepted Dogecoins or Bitcoins, or was acquired by a SPAC (Special Purpose Acquisition Company), its current valuation would seem like child’s play.

In fact, I think I could probably spare the time it usually takes you to read my less than pithy quarterly updates by simply providing you with a bunch of other headlines from the last few months, which really articulate the state of the real estate market, at least when it comes to single-family homes:

- “A $400,000 House Got 122 Offers in Two Days,” Wall Street Journal

- “Home Prices in Southland Rise 14.5% Amid Feeding Frenzy,” Los Angeles Times

- “Home-price Surge Hits 15-year High,” The Real Deal

- “More Real Estate Agents Than Homes for Sale,” Wall Street Journal

Meantime, multifamily real estate brokers echo similar sentiments when discussing the apartment market. One Georgia-based broker told us that they had received 25 “serious” offers on one project and the “winner” was a group out of the Pacific Northwest, which outbid all competing offers by some $2 million, surprising even the brokers themselves.

In Arizona, deals are trading anywhere from five to 15 percent above asking price. Brokers are consistently receiving at least 30 offers on projects, with over 10 invited to the “best and final” stage. Such offers routinely include large (e.g., “7-digit”), non-refundable deposits. I recently visited Phoenix and virtually every apartment project I visited had no vacancies whatsoever. If the two-hour wait time to rent a car from Thrifty Car Rental is an indication, Phoenix’s attractiveness as an investment destination will persist for some time.

The story is the same elsewhere, from Idaho, to Utah, to Colorado, to Texas, to North Carolina. These anecdotes reflect why we are so interested in acquiring assets in these markets, but at the same time we must be especially thoughtful and conservative in our underwriting and negotiations. It is really not surprising that we routinely find ourselves left at the altar and unsuccessful in those “best and finals.” For every project in which we successfully reach the finish line, there are countless other times in which we are simply outbid.

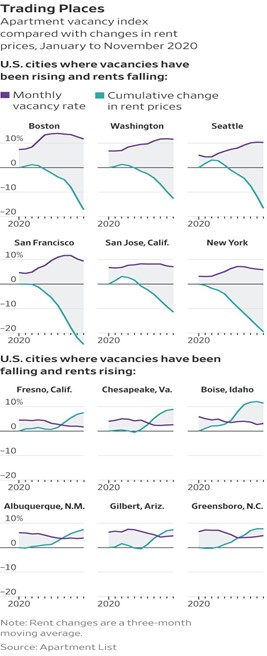

Then again, to show how unique individual markets are, anyone who acquired residential rental property in New York City in the last 10 years is probably under water, likely having lost anywhere from 40 to 50% of their equity because of sharp declines in rental rates and increases in vacancy rates over just the past 12 months. I can almost hear the lyrics to that Eagles’ song from many moons ago: “In a New York minute, everything can change. In a New York minute, things can get pretty strange.”

While perhaps a bit of an “eyechart,” I found the following to be very informative, summarizing rent and vacancy statistics and changes across many cities in the U.S. between January and November of 2020, consistent with the perspective I just expressed:

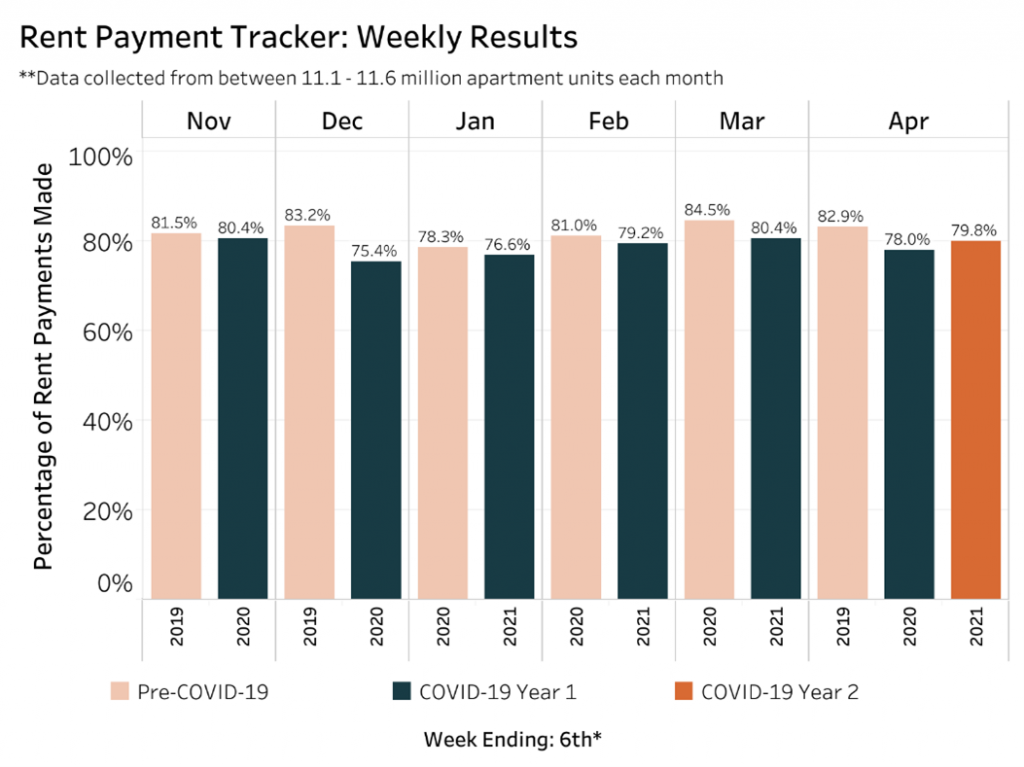

Overall, the apartment market has stabilized in the past few months, but delinquencies remain stubbornly high. While applications, move-ins, and lease renewals are rising, nearly six percent of residents across the U.S. have rent balances outstanding in excess of one month, and on average, such residents are behind some 3.5 months on their rent. Nearly two percent of apartment residents are five or more months behind in their rent. Across the Clear Capital portfolio, we are experiencing similar results, though not surprisingly delinquencies vary across projects and locations. The following summarizes overall collections across the country, according to the National Multifamily Housing Council:

In any event, I have not seen any market quite like this, which shares distinct similarities to 1998 to 1999 and 2005 to 2007, when certain asset prices seemed profoundly disconnected from underlying fundamentals. How else can one justify the values of Dogecoin (a cryptocurrency competing with Bitcoin), GameStop, many SPACs, or that now world-famous New Jersey deli, among numerous other examples?

However, with a post-COVID economic recovery under way, historic levels of government stimulus (including the $1.9 trillion COVID relief plan passed this quarter), 10-year Treasury yields below 1.60%, record-levels of liquidity, and bank balance sheets in seemingly decent shape (a total of about 20 banks have failed in the last five years versus over 300 between 2010 and 2013), this time feels quite different from those two other auspicious timeframes, and I am more concerned about inflation than I am about a broad market downturn, as I have written about previously. In fact, consumer prices rose sharply in March, up 2.6%, which hardly sounds alarming, though it represents the largest increase since August 2018, so stay tuned.

In summary, the first quarter was extremely eventful, with some very wild market moves, even capturing the attention of investment stalwarts like Paris Hilton. Residential real estate prices increased sharply, which may be one of the most significant stories of the quarter, whose impact will reverberate for some time to come. Oh, and did I forget to mention that UCLA’s men’s basketball team made it to the Final Four in the NCAA Tournament, before losing at the buzzer on a 45-foot bank shot? In overtime? As a double-digit underdog? Or the Capitol riot of January 6th and the inauguration of President Biden?

Indeed, it was that kind of quarter.

Secondary and Tertiary Markets, Especially Those in the Southwest, Sunbelt, and Mountain West, Continue to Lead

Continuing a trend which has persisted for some time, the hottest real estate markets include markets like those mentioned above: Boise, Fresno, Greensboro, Gilbert, Riverside, Albuquerque, Tucson, and Memphis, where rents have increased anywhere from nine to 12% over the past year. Across the entire country, in the 134 markets in which data is available, rents were up very modestly in the past year, some 0.6%, and 0.8% during the quarter. Of course, these higher rents are not completely uncorrelated to both resident delinquencies and the inability to evict such residents, which artificially reduced available supply.

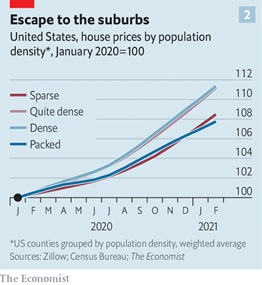

However, the demographic diaspora from the Coasts to less expensive and more suburban markets has been impactful. According to Zillow, some 10% of Americans relocated during the pandemic, with Phoenix, Charlotte, and Austin leading the top destinations. As one Austin homeowner put it, “They just keep coming. The fleece vests, the tech bros. That’s definitely imported from California.” Austin has been the fastest growing city in the last decade, growing 30%, with half of the growth representing Texans relocating from other parts of the State to Austin.

Home prices increased in all of the 100 largest metros in the U.S., according to Zillow. However, in some of the wealthiest, tightest residential markets – San Jose, Seattle, NY, Boston, Austin, SF, DC, LA, Chicago – rents declined, in some cases by more than 10%. The dichotomy is noteworthy, where home prices have increased while rents declined, both by double-digits. I am not sure this has ever occurred, certainly not in my memory.

Perhaps another anecdote may be illustrative, this time involving a close friend, who relocated from West Los Angeles to Lexington, South Carolina, a quiet suburban neighborhood about 15 miles outside Columbia, the state capital. As a personal trainer, the pandemic forced him to provide services remotely, and with products like Peloton and other products (e.g., the “Mirror” from Lululemon) providing in-home, yet interactive, workouts, it is clear that personal trainers and the like can live virtually anywhere and still engage with clients. Not only are all gyms at great risk (that may be an understatement), but suburban housing markets have found a new source of demand. COVID has made it clear that certain jobs can be performed almost entirely via FaceTime or Zoom. His brother, a local realtor, is receiving dozens of offers on every home he lists, and on one transaction, he received a most unusual proposal, which offered to pay “$1,000 above any other offer received,” all cash, with a quick close. Again, I had never heard of an offer quite like that one, and this is for a single-family home in Lexington, South Carolina, population of less than 23,000.

A recent article in the Wall Street Journal noted that some suburban homebuyers are actually foreign investors, stating that “blocks of families are sending monthly rent checks to ventures backed by Canadian pension funds, European insurers, and Asian or Middle Eastern government-run funds.” Supposedly up to a third of institutional investors in single-family residential properties are foreign. In fact, just last week, the German insurer, Allianz SE, said that it is investing $4 billion in U.S. rental homes, as if prospective homebuyers need additional competition.

In short, I anticipate continued growth in the same markets that have been leaders in recent years, those secondary, tertiary, and even quaternary locations (yep, including red-hot Fresno), with the biggest unanswered question whether supply can keep up with demand. As discussed in more detail below, my sense is that it will be a challenge (read: perhaps impossible) to do so in many of these markets.

With Substantially Higher Commodity and Construction Costs, Widespread NIMBYISM (Not in My Backyard), Poorly Construed Public Policies, and Broadly Insufficient Supply, Housing Prices – Both Single- and Multifamily – Are Not Likely to Moderate Anytime Soon Even if Demand Moderates

In a recent memo and/or podcast episode I recorded (“Focus on Facts, available at Spotify and Apple Podcasts, admittedly some shameless self-promotion), or perhaps both, I indicated that those hoping for lower home prices would be “waiting for Godot” because of the severe imbalance between demand and supply in nearly every market. According to Freddie Mac, the U.S. housing market is nearly four million homes short of what is needed to meet demand, a 52% rise from 2018, when they first began to estimate and quantify the shortfall.

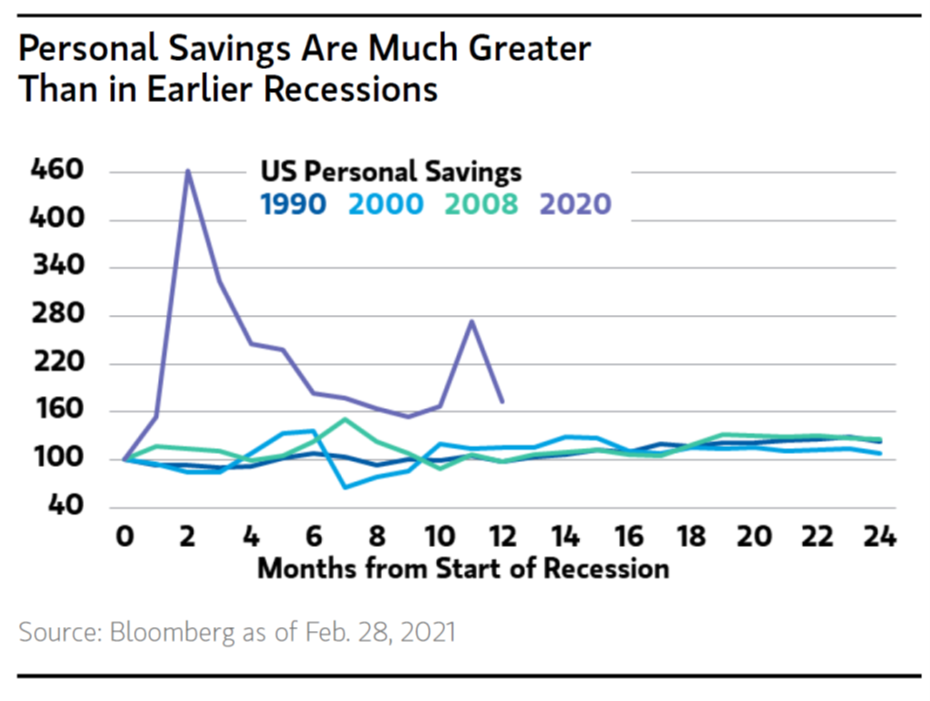

Historically low rates, unprecedented liquidity, COVID and related stimulus, institutional and foreign purchasers, record number of Millennials (30 to 39-year-olds) in search of permanent housing and perhaps experiencing FOMO (Fear of Missing Out) are driving unprecedented demand for homes. Imagine that on nearly every successful transaction, there are anywhere from ten to 150 bridesmaids or groomsmen, unsuccessful bidders who will likely be bidding on the next home available for sale. With personal savings having accumulated over the past year of COVID, significant dry powder awaits both increased consumer spending and investment.

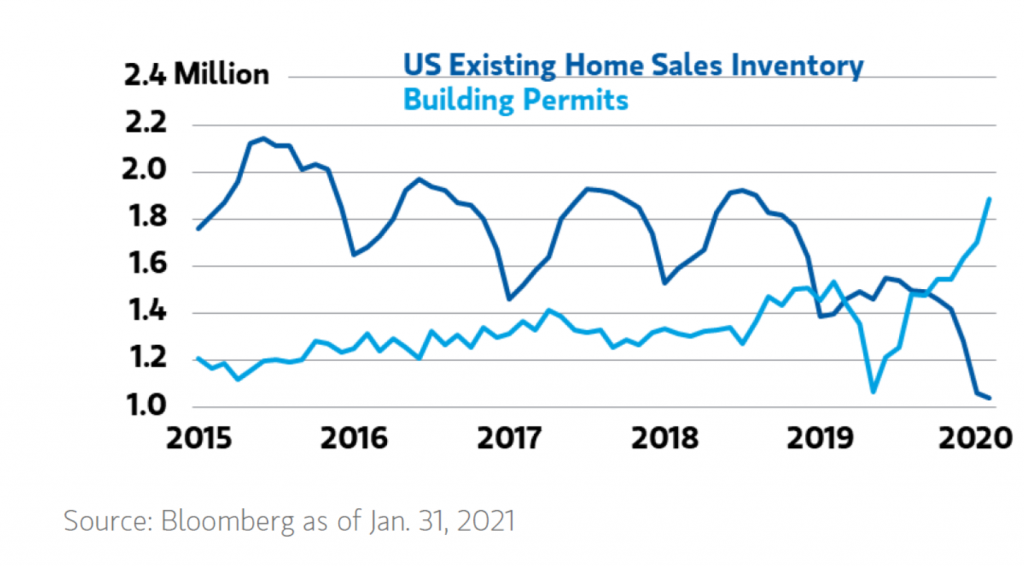

Meanwhile, the supply of homes for sale remains at record lows. For example, there were about 1.3 million homes available for sale at the end of 2020, representing about 2.3 months of supply, down 22% from the prior year. Perhaps my very favorite (if not sobering) statistic revealed this quarter, in late March, was that real estate agents outnumber homes for sale nationwide. At the end of January, one month later, some 1.04 million homes were available for sale, down 26% from the prior year and the lowest on record since 1982, while there are 1.45 million licensed real estate agents nationwide, up nearly five percent from the prior year.

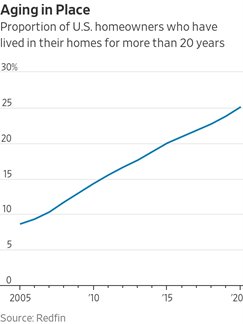

While countless renters have relocated during the pandemic, homeowners are mostly staying put, especially Baby Boomers with their $10 trillion of equity, impacted by COVID and unfavorable tax policy (capital gains). According to Redfin, the typical homeowner in 2020 had remained in their homes an average of 13 years, up slightly from 12.8 years in 2019, but far longer than in 2010, when homeowners had lived in their homes an average of 8.7 years.

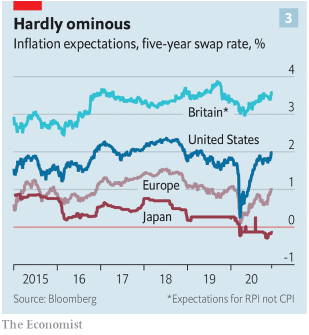

While not concerned about increased debt levels in the short-run, as mentioned, I do fear the higher inflation and asset values they will likely fuel in the intermediate to longer-term. I don’t think for a second that the Fed’s “easy” monetary policies and elevated equity values are unrelated. However, at this point, the markets are not forecasting significantly higher inflation. It may just be that inflation in financial assets (including real estate) will be offset by broader deflation in everything from energy to consumer goods to office and retail rents.

A recent Los Angeles Times article highlighted the challenges, perhaps particular to California, noting that not a single of the more than half dozen bills introduced last year to address the state’s housing crisis was passed, in large part “because of campaigns waged against them by the state’s powerful construction-workers union.” Union opposition is one of the principal reasons politicians have been unable to pass legislation streamlining and accelerating construction approvals and easing zoning restrictions. The irony is not lost on me. The sorts of individuals who would probably benefit significantly from lower rents and housing prices – blue-collar individuals who work in the construction trades – stymy new construction and exacerbate the problem. Is it any wonder that it costs as much as $700K to construct an “affordable” unit, perhaps double what it costs to build a comparable market-rate unit?

Meanwhile, local opposition to building is so commonplace and the approval process so cumbersome, time consuming, and expensive, even when a proposed project complies entirely with requirements, approvals are not forthcoming, at least in an expeditious manner and needed supply is simply not provided. Recently I heard of a new acronym to add to my vocabulary: CAVE, Citizens Against Virtually Everything, to be added to NIMBYISM and BANANA (Build Absolutely Nothing Anywhere Near Anyone).

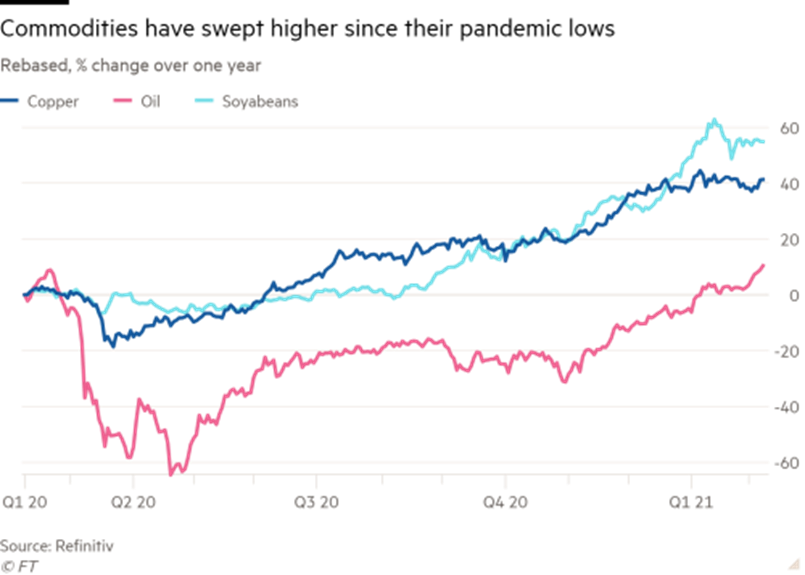

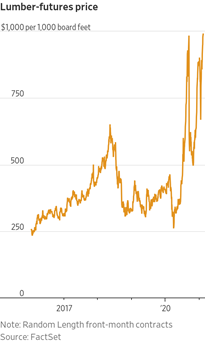

Finally, commodity prices continue to climb, or “go through the roof,” as it were. Crude oil, the key component of everything from paint to drain pipes to roof shingles to flooring, has increased 80%, yes 80%, since October. Copper, used extensively in both plumbing and electrical work, costs roughly a third more now than it did a mere six months ago. Prices for everything from insulation, granite, concrete, and brick reached record levels this year, according to the Bureau of Labor and Statistics. Drywall and ceramic tile prices have also increased, while significantly higher lumber prices have added something like $24,000 to the cost of an average home and $9,000 to an average apartment. Ouch. According to PulteGroup, Inc., one of the largest homebuilders, the average cost to construct a home in the fourth quarter alone was up 7%. American Homes 4 Rent, which constructed some 1,600 units last year and plans to build another 2,000 in 2021, said it spends between $20-25,000 per unit for lumber, more than double what it spent last year.

Lest you think this is merely a U.S. phenomenon, it is not. In the 37 countries in the OECD (Organization for Economic Cooperation and Development), home prices hit a record last year, up five percent, the most in nearly 20 years. From Bicester in the U.K. to Omaha, Nebraska, to Berlin, home prices are rising, up 11% year-over-year here in the U.S., 8% in the U.K., and 9% in Germany.

While Treasury and Mortgage Rates Rose During the Quarter, They Remain Low by Historical Standards. However, Higher Inflation Remains a Real Risk

During the first quarter, interest rates increased, and not insignificantly, at least in relative terms. At the start of 2021, the yield on ten-year U.S. Treasuries was 0.93%, and at last glance, 1.56%, while average 30-year mortgage rates had increased from about 2.7% to nearly 3.1% today. However, the increase has negligibly impacted demand, best I can discern.

One big question mark is how long the Federal Reserve can wait before it decides to raise rates. According to Morgan Stanley, recent data implies a rate hike in 20 months or so, which essentially comports with Fed Chair Jerome Powell’s public statements.

Clearly some increase in inflation was inevitable given the collapse in consumer spending and demand following the COVID outbreak, but March’s increase in inflation to 2.6%, up from February’s 1.7%, represents the most significant rise since 2009. Inflation will soon surpass the Fed’s two percent target (it uses a different index), but the Fed will truly be engaging in a tricky balancing act worthy of Cirque d’Soleil.

Economic recoveries produce price pressures and the impetus for higher interest rates and the post-COVID recovery will certainly be no different. On the other hand, higher interest rates can and will dampen economic demand for capital investment and other goods and services, and could threaten any economic recovery, so the Fed will be trying to walk a fairly narrow tightrope between now and the next 12 months.

Even in Quarantine, Elected Officials Have Been Busy

One of the things that will be fascinating to watch, and track is how governments at every level and across the globe continue to intervene in housing markets, as they try and protect renters from eviction, homeowners from foreclosure, all while trying to increase the stock of affordable housing and address ever increasing homelessness. However, their efforts seemed doomed, at least in the longer-term, as they lack the political will and financial resources to do so.

Meantime, the CDC has extended its eviction freeze through June 30 and state and local governments will be moving aggressively to shore up their fiscal deficits, resulting from significant declines in tax revenues because of the pandemic. Nashville instituted a 35% surcharge on property taxes last year, and Lord knows how New York City plans on dealing with its $9-10 billion projected budget deficit. Knowing politicians, they will likely choose some profoundly suboptimal policies, but those that are palatable to constituents. Let me go out on a proverbial limb to predict that higher local and state taxes are likely coming down the pike.

As moratoriums surrounding the eviction of residents and foreclosure of homeowners behind in their mortgage payments expire, we will have to see how landlords, lenders, and the Courts respond. I imagine many landlords and lenders will work with residents and homeowners to minimize losses and manage vacancy rates, while working aggressively to collect delinquent rents and mortgages. On March 11th, the latest COVID relief bill, the “American Rescue Plan Act” was passed into law, a $1.9 trillion relief package that includes $50 billion in housing resources, including some $27 billion for rental assistance. Combined with $25 billion in rental assistance provided by Congress last year, over $50 billion is available to assist struggling renters and landlords who have also been impacted, including Clear Capital. How quickly these funds will be distributed by individual states remains to be seen, and Clear Capital, like nearly every landlord, are understandably eager to collect as much of the nearly $2.5 million in delinquent rents we have experienced across our entire portfolio as we can.

Meanwhile, across the Pond, you may recall that Germany passed a five-year freeze on residential rents back in 2019 that prevented owners of any property built before 2014 from raising rents, the most onerous rent control regulation I have ever seen. And the preliminary results are in. According to German Institute for Economic Research, rents for units built before 2014 are in fact down 11% as compared with those that are not regulated, but, as any economic analysis would have predicted, the Country’s housing shortage has worsened. The number of units available for rent has declined by more than 50%, as tenants are hanging on to their rent-regulated units with both hands, while in other cases, landlords are using units for themselves, selling them, or keeping them vacant in hopes that the Courts determine the law is unconstitutional. All these outcomes were entirely predictable to anyone with even the most basic training in fundamental economics.

Finally, and as usual, a few other noteworthy tidbits have caught my eye during the quarter

As usual, I would be remiss if I neglected to mention a couple other tidbits or relevant data points that might be of interest.

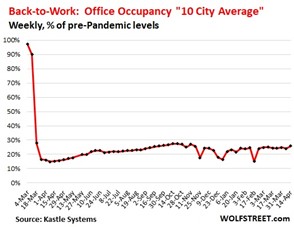

- Significant Office Vacancies are Likely to Persist for an Extended Period of Time: Not surprisingly, office vacancies are piling up and in historic fashion, and I believe the slump will be long-lasting. From Houston to San Francisco to Los Angeles to Manhattan to Chicago to D.C., things are particularly ugly. In the ten largest metros, office occupancy is only 26% of pre-pandemic levels, according to Kastle Systems, whose electronic access systems are found in thousands of office buildings throughout the U.S.

- While hotels focused on leisure have already seen a modest recovery, convention-reliant hotels are in a world of hurt and won’t bounce back for some time: For the first time in nine months, I traveled recently, to Phoenix, as I mentioned earlier, to visit a new project we are acquiring, Urban Park, and an asset we acquired a couple of years ago, Aspire Glendale. Both LAX and Sky Harbor, Phoenix’s airport, were fairly busy, at least the Southwest terminals. The flights were entirely, or nearly entirely, full. Activity at the rental car counters was what I would have expected to see before COVID, and in fact, busier.

According to recent data from the Bureau of Labor and Statistics, the leisure and hospitality industry led last month’s job gains, adding 280,000 jobs in March, following the addition of 355,000 jobs in February. A recent poll indicated that some 87% of households plan to travel in the next six months, up from 60% just a couple of months ago. Obviously COVID hit the travel and tourism industry with a stiff uppercut, but the industry is in recovery mode and pent-up demand, significant. Full recovery is still a couple of years away, I would think, especially in international travel. And leisure hotels will fare far better and recover far more quickly than those that rely more heavily on conventions and conferences.

A couple of specific data points may be probative. Hilton had reopened 97% of its hotels as of February 10th. Of the 989 licensed casinos in the U.S., 935 have now reopened. However, it should also be noted that Nevada is limiting occupancy at reopened hotels to 35% occupancy until June 1st, when the State intends to completely reopen. In California, rules vary by county, but the State intends to reopen on June 15th. We shall have to wait and see, but fingers and toes are crossed. I can tell you that Clear Capital intends on holding its annual staff meeting in-person this year, in October, if all goes to plan.

In any case, I don’t foresee substantial foreclosures in the hotel/hospitality space, as lenders don’t want to take back these assets and have learned their lessons from prior downturns. It is usually best to work with borrowers to maximize recoveries and outcomes.

- The Retail Industry is the One that May Never Recover, at Least in Some Segments: It is a secret to absolutely no one that retail faced significant challenges and headwinds before COVID, and I have routinely, if reluctantly, provided data on store closures and retail bankruptcies in nearly every quarterly memo. 2020 saw a record of permanent retail closures, with over 12,000 stores closing their doors.

So what’s the post-COVID retail reality look like? That remains a big question mark, as I can’t imagine how large indoor malls, anchored not just by “big boxes,” but movie theatres will fare. We have all gotten used to watching everything, including first-release films, from the comfort of our couches. Between higher-quality, large screen, smart TVs, surround sound, and decent homemade popcorn, we are more willing to enjoy movie fare at home. I just don’t see movie theatres being able to remain open for some time. I recently read that Los Angeles-based Pacific Theatres, parent company of ArcLight, announced that the company has decided not to reopen any of its theatres. And larger chains like AMC, and the malls in which they operate? I think they face profound headwinds, and sadly, I anticipate that I will be reporting additional sobering statistics on retail assets looking forward.

While the Next Six Months Will Bring a Much Stronger Economy, the Recovery will be Uneven, with Anticipated Fits and Starts. Residential Real Estate Will Continue to Fare Well, but Cautious and Conservative Underwriting Must Accompany Any Acquisitions

The last 13 months seem almost surreal, and somehow, I could not have said it any better than Jerry Garcia and the Grateful Dead, “What a Long Strange Trip it’s Been,” even though the trip is not quite over. However, we are certainly over the hump, though there will be fits and starts, and perhaps a spike here or spike there, a variant there, and variant here. That is not to make light of any sort of possible resurgence, and I am sure the media will do its part to engage (read: scare) us during this period of time. But the reality is that the next six months will bring significant increases in economic activity, travel, and employment, terribly uneven as they might prove.

Meanwhile, residential real estate, both single- and multi-family assets, will continue to perform very well, as delinquent rents are recovered, evictions resume, the job market recovers, and a slew of 20-35 year olds vacate their parents’ basements or old bedrooms, and enter the rental market. The demand-supply imbalances I discussed above and in previous missives will persist for the foreseeable future, and the private sector can only do so much to address a widespread public policy challenge.

Finally, you may have already received information about our latest offering, a 104-unit project in Phoenix, Urban Park Apartments, which offers compelling cash flows and upside as we increase rents to market and execute our value-add strategy to the Project. I hope you might join us in the opportunity. Meantime, we anticipate other offerings in short order, as we scour the Southwest, Sunbelt, and Mountain West regions for opportunities. Stay tuned!

Thank you for your continued support of our firm and its endeavors.

Best,

Eric Sussman